Приобрети журнал - получи консультацию экспертов

№1(12)(2013)

Previous article was devoted to the peculiarities of audit of leased state property initiated by the State Property Fund of Ukraine upon prolongation of such lease agreements. These peculiarities are due to the fact that the state should carry out continuous monitoring of not only the completeness of paid lease amounts for the duration of lease agreement, but also for improving the conditions of fixed assets, i.e. the use of amounts of accumulated depreciation.

Last time we discussed three main objectives of auditing leased IPC. The fourth task of the audit is confirmation by the auditor of registration of a leased fixed asset (state property) after evaluation of leased integral property complex.

It should be noted that upon prolongation of the lease of state property it is required to conduct valuation of leased IPC. Valuer as a subject of valuation activity must act on the basis of of Valuer's Certificate. They conduct an independent valuation of fixed assets (buildings, structures, networks, equipment and vehicles) leases by the company. When conducting valuation according to the accepted norms, comparative, revenue and cost approach are used. The purpose of valuation is to determine the market value of the property for accounting.

Upon the results of valuation the market value of fixed assets (buildings, structures, networks, equipment and vehicles) of the company for all groups is determined. The auditor should verify the correctness of the accounting of revaluation surplus amount of the object of fixed assets (leased integral property complex) of the enterprise.

In accordance with paragraph 17 of the Order of the Ministry of Finance of Ukraine № 92 of 27.04.2000 "On Approval of IAS 7 "Fixed Assets", revalued historical cost and depreciation amount of fixed assets is determined by multiplying the historical cost and the depreciation amount of fixed assets by the index revaluation. Revaluation index is determined by dividing the fair value of the object that is revalued, by its net book value.

If the residual value of a fixed asset equals zero, its revalued residual value is determined by adding the fair value of the object to its original of revalued) cost without changing the amount of depreciation of the object, and for these objects that continue to be used , recovery value is always determined.

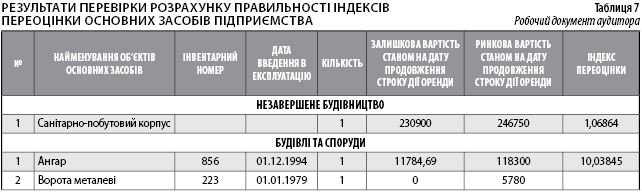

The auditor confirms that accounting for for the amount of revaluation of property leased integral properpty complex, the enterprise has correctly calculated the indices for each revaluation of fixed assets. Results of testing the accuracy of index calculation of revaluation of fixed assets are drawn up in audit working paper (for example in Table 7).

Table 7

Audit Working Paper

Results of checking the correctness of the calculation of indices of the Company’s fixed assets revaluation

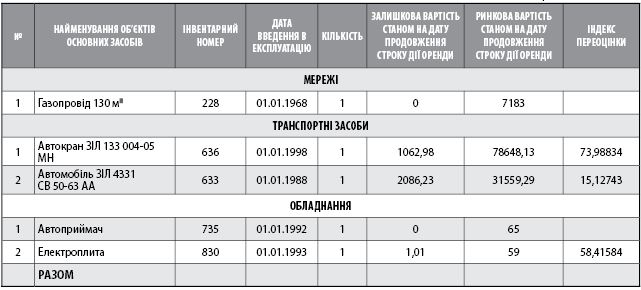

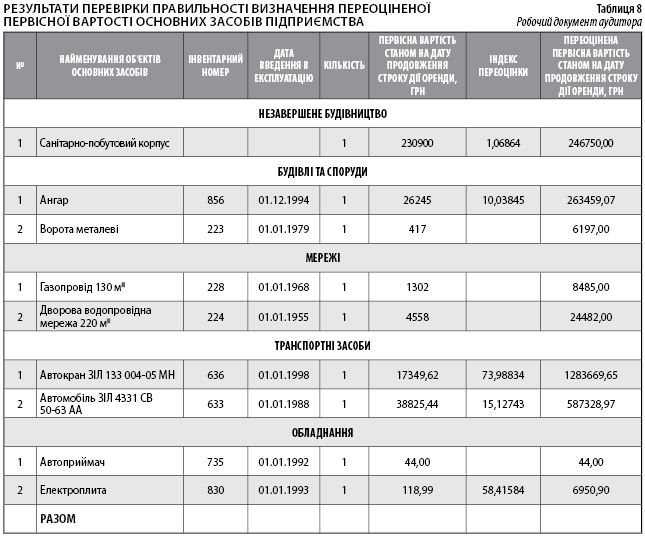

After receiving information about the calculation of indices of revaluation of leased fixed asset objects the auditor carries out confirmation procedures of revaluation of fixed assets. They must verify correctness of estimated revalued historical cost and amount of depreciation by arithmetic means - multiplying the revaluation indices by the the original cost and amount of depreciation.

Example of conducting and presentation of revalued historical cost is shown in Table 8.

Table 8

Audit Working Paper

Results of testing the accuracy of determination of the revalued original value of fixed assets of the company

The revalued amount of depreciation is calculated similarly, thus the auditor may confirm the company has done it accurately (Table 9).

Table 9

Audit Working Paper

Results of testing the accuracy of determination of the revalued amount of depreciation of fixed assets at the company.

The auditor obtains information and verifies the manner of presentation accounting of revaluation of fixed assets. According to NAS 7 , the amount of revaluation surplus of the residual value of fixed assets is included in the additional capital, and the amount of markdown - in the costs. The company must show revaluation surplus amount in the subaccount 423 "Revaluation of assets." The increase in initial cost is shown in accounting entries:

Dt 10 "Fixed Assets" Ct 423 "Increase in value of assets"

and increase in the amount of depreciation

Dt 423 "Increase in value of assets" Ct 131 "Depreciation".

Information about changes in initial cost and the amount of depreciation should be entered in the the registers of analytical accounting.

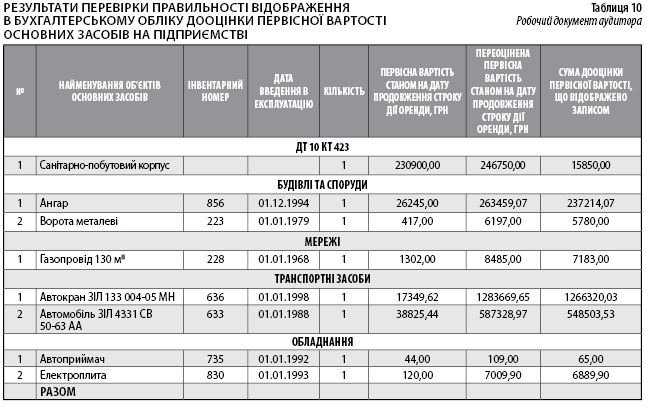

Results of testing the accuracy of recording in accounting records of revaluation surplus of the original value of fixed assets at the company are to be formalized in the audit working paper example of which is presented in Table 10.

Table 10

Audit Working Paper

Results of testing the accuracy of accounting for revaluation surplus of the original value of fixed assets at the company.

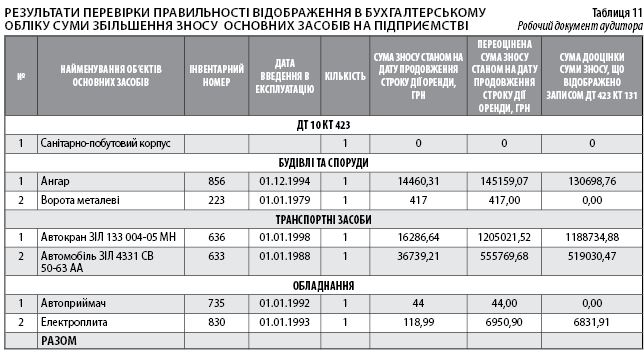

Example of testing the accuracy of accounting for increased amount of depreciation is presented in Table 11.

Table 11

Audit Working Paper

Results of testing the accuracy of accounting for increased amount of depreciation in the company.

In our opinion, such manner of recording in the accounting of revaluation surplus of fixed asset objects (leased integral property complex) has shortcomings in terms of determining the initial value and the amount of depreciation for individual objects, the amount of which is shown in the balance sheet.

Thus, when specifying in the accounting of revaluation surplus amounts we apply index of revaluation, to which increase both the initial cost and the amount of depreciation. For example, the residual value of an electric cooker (commissioned in 1993) prior to revaluation was 1.01 UAH, following revaluation it should be 59.00 UAH. Thus, the index of of revaluation amounts to 58.41584. After a simultaneous increase in initial cost of 120,00 UAH, and the amount of depreciation 118.99 UAH for index of revaluation, revalued initial cost amounts to 7009.90 UAH and revalued amount of depreciation – 6950.90 UAH, so that residual value makes 59.00 UAH. If we show in such manner in the accounting the amount of revaluation surplus of fixed asset objects (leased integral property complex) that have a residual value, initial cost of such fixed assets is increased by a significant amount, which does correspond the market value of the objects . Thus, the indicators of the company's balance sheet in part of their cost are distorted.

Stating in the accounting the revaluation surplus of fixed asset objects on which zero residual value is calculated, increases only initial cost to the market value of fixed assets. In our example, when the electric cooker (commissioned in 1993) had a residual value of zero, after revaluation the initial cost should amount to 59.00 UAH.

In our view, it is necessary to change the manner of stating in the accounting of amounts the revaluation surplus of fixed asset objects , and reflect only increase in the initial cost to the amount of the market value of the object.

For example, the initial cost of an electric cooker ( commissioned in 1993) which prior to revaluation was 120.00 UAH, after revaluation should be 179.00 UAH. So, the residual value of the asset after stating equals the market value in the amount of 59.00 UAH. In applying this manner of stating amounts of revaluation surplus of fixed asset objects (integral property complex) the initial cost will increase by the amount of the market value that will appear in the balance sheet.

Considering the specific tasks during the audit of companies that prolong the lease of state property (IPC), we believe that the State Property Fund of Ukraine should approve recommendations on disclosure of information in the audit report. This is especially true for fixed asset objects, determination of their initial, residual and market value, confirmation of calculation of unused amounts of depreciation and the procedure for this calculation.

Головне