Приобрети журнал - получи консультацию экспертов

№2(13)(2013)

Sovereign credit ratings of Ukraine lowering in December 2012 has attracted public attention and caused number of assumptions and estimations about future economic development, its investment appeal. However, not everyone thinks over criteria that affect ratings formation. Vasyl Bashko (PhD) talks about rating methodology and reasons for low credit ratings of Ukraine

How Standart & Poor's determine their ratings?

- Standart & Poor's characterizes default as failure of principal or accrued interest repayment on obligations on date or within specified in original contract period. Default describes also cases of exchange commitments to new with worse conditions, without paying adequate compensation. "Worst conditions" include reduction of principal amount, increasing maturity, lower rate, currency or other additional conditions for issuer benefit. According to the Standart & Poor's method, even slight difference between nominal maturity of obligations to be exchanged and new commitments can be considered as restructuring. In this case, specified bond rating drops to Category D, and ratings Issuer credit rating – to category SD.

Usually exchange obligations are not treated as default case. However, when there are concerns among investors about high probability of default and downgrade of sovereign rating, it is difficult to determine whether such an exchange took place on voluntary conditions.

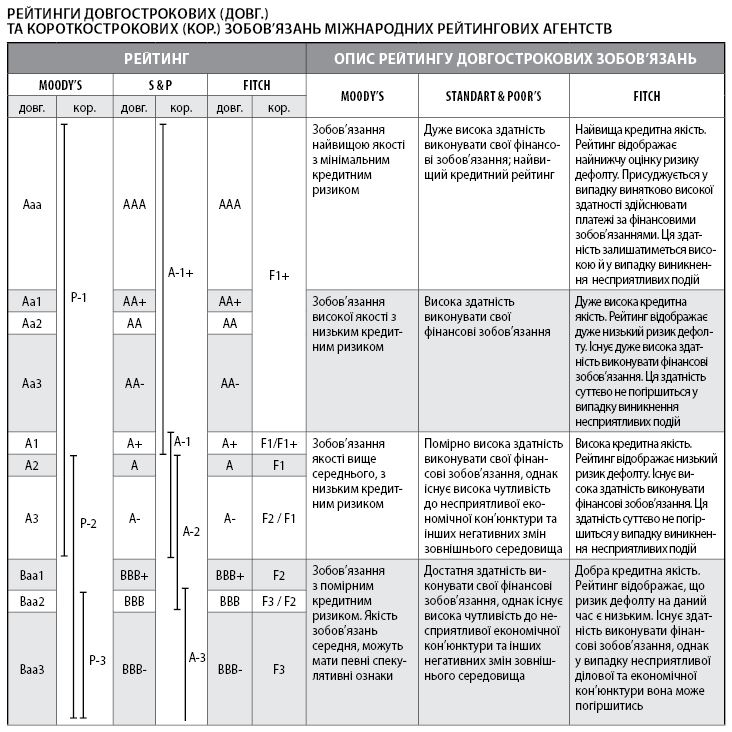

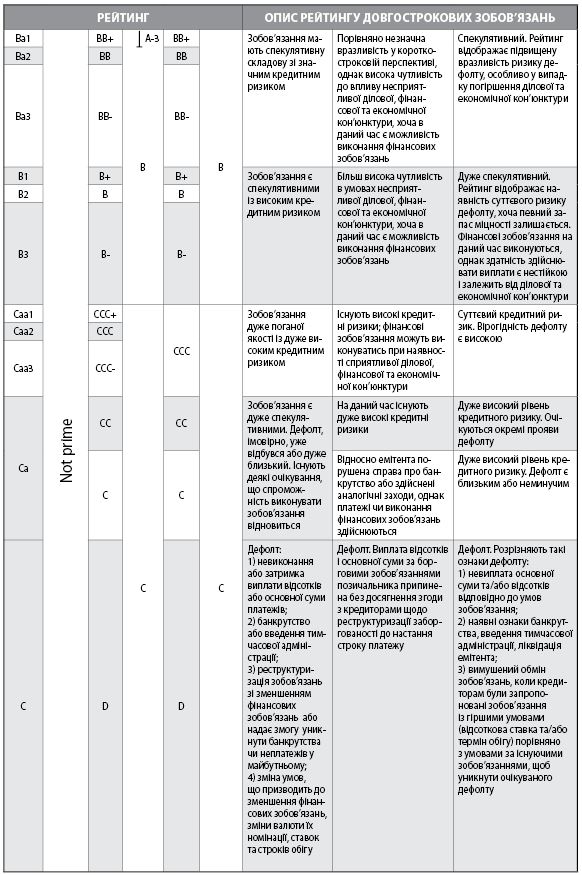

Table 2. Ratings of long-term (long) and short-term (short) obligations for international rating agencies

Consent for exchange may be caused by expectations of default in case of failure of this "crisis" exchange. When deciding whether particular case refers to "crisis" exchange, Standart & Poor's assesses how likely is traditional default (non-payment) for obligations that are exchanged in short and long run. It takes into account current bond rating to be exchanged:

1) if the Issuer credit rating is at level of B- or lower, this exchange is considered a "crisis" or restructuring;

2) if the Issuer credit rating stands at BB- or higher, this exchange is not considered a "crisis" or restructuring;

3) if the Issuer credit rating is at the level of B + or B, decision to classify agreement as restructuring is taken basing on quotations of bonds to be exchanged, and those on that exchange.

Overall assessment of creditworthiness of sovereign issuers is based on analysis of political and economic risks and requires consideration of qualitative and quantitative evaluations. Factors of economic activity are measured by quantitative indicators, while political risks, socio-economic strategy are evaluated qualitatively. In particular, one of the factors is willingness to pay own obligations. When lenders are unable to fully meet their legal requirements, the government on selective basis can refuse to perform its obligations, even when there are financial opportunities to service debt on time.

In practice, political and economic risks are related. The government is not willing to pay its debts generally pursued an economic policy that reduces its capacity in this regard. Thus, willingness to pay is result of series of economic and political factors influencing public policy.

Despite the fact that ability and willingness of government to fulfill debt obligations in national and foreign currency depend on same political and economic factors, extent of this influence is different for quantitative traits. Ability and willingness of national government to service and repay debt in local currency is maintained by its tax policies and ability to control national monetary and financial system, which gives almost unlimited access to resources in national currency. However, in order to service public debt in foreign currency, the government should buy it - usually in foreign exchange market. In some cases it may be an insurmountable obstacle, as evidenced by much higher prevalence of default on obligations in foreign currency than local.

In process of credit analysis on liabilities in national currency Standart & Poor's primarily examines economic strategy of government, especially its monetary policy, as well as plans for privatization and other reforms in microeconomics and additional factors that can strengthen or weaken incentives for timely debt service and repayment. Analyzing risk of sovereign default on liabilities in foreign currency, agency is studying impact of these same factors on balance of payments and external liquidity indicators, as well as size and characteristics of external debt.

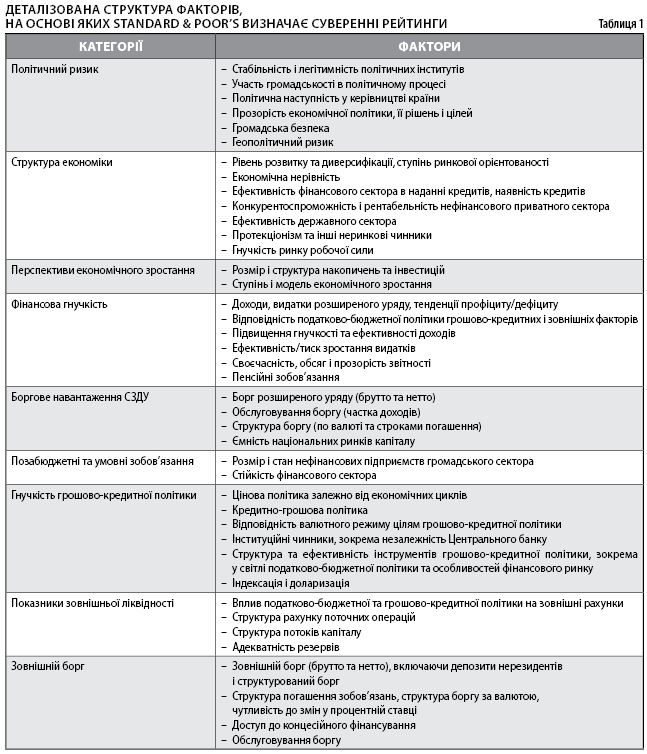

Standart & Poor's considers main economic and political risks when determining ratings of sovereign debt, namely: institutions and trends of political development and their impact on efficiency and transparency in terms of economic policy and public security and geopolitical issues, structural organization of economy and growth prospects; revenues flexibility for expanded government and factors that have pressure on costs, deficit of expanded government and debt load, amount of contingent liabilities in financial system and public sector, flexibility of monetary sphere, external liquidity and trends in government obligations and private sectors to non-residents (Table 3).

First four factors directly affect ability and willingness of governments to provide timely service and repaying debt in local currency. Since fiscal and monetary policy ultimately has impact on external balance of payments, fourth and fifth of the above factors also affect ability and willingness of governments to provide timely service and repaying debt in foreign currency. Among the most serious factors are those associated with state of balance of payments.

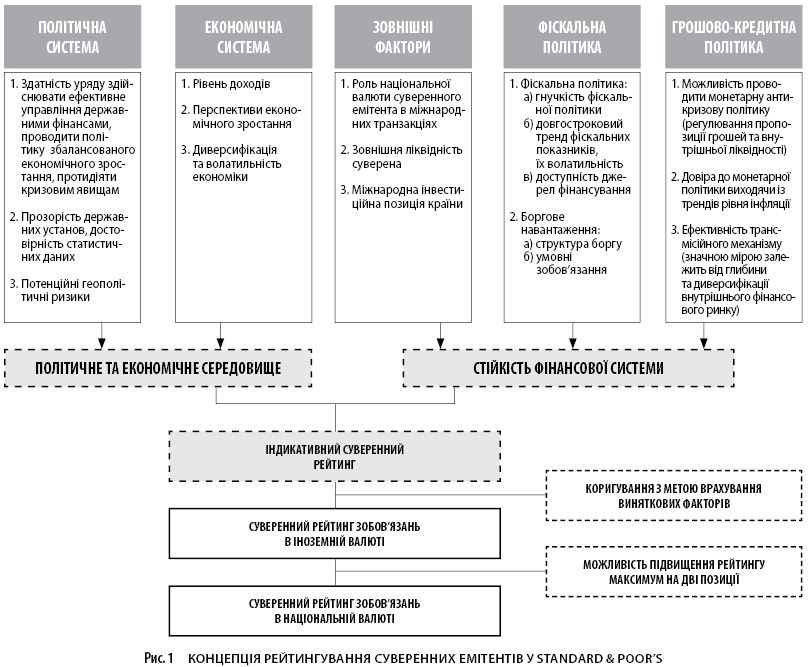

In July 2011, Standard & Poor's upgraded rating methodology on sovereign issuers. New algorithm, in particular, requires consideration of state contingent liabilities related to financial sector, and special approach to sovereign issuers, countries which are members of monetary union. More attention is paid to factors that may affect intentions and capabilities of sovereign issuers to service debt obligations timely and fully. Dynamics of economic and political cycles, fiscal and monetary flexibility in terms of future economic cycles are taken into account. Main five factors considered in credit analysis of sovereign issuers are displayed in Fig. 1.

Based on quantitative indicators and qualitative assessments all relevant factors are awarded points from 1 (best result) to 6 (worst). Further mean scores measures for political and economic environment are displayed, as well as the financial system stability. Rating scale for political and economic environment is divided into 11 points and increases uniformly by 0.5 points. Instead the scale of financial system stability is divided into 9 points and increases nonlinearly. On this basis, the "indicative rating level" is determined which usually corresponds to sovereign rating of liabilities in foreign currency. Matrix with scale of scores measuring political and economic environment and financial system stability on which S&P awards sovereign ratings, is reflected in Table 4.

Fig. 1. Concept of sovereign issuers rating in Standard & Poor's

How Fitch methodology for ratings determination is different?

- Issuer Default Ratings reflects assessment of ability and willingness of state to fully and timely meet its current and future obligations. Sovereign issuers are assigned three types of issuer default rating: in foreign currency on long-term and short-term obligations and in local currency on long-term debt. According to Fitch, short-term debt obligations in local currency are assigned as long-term ratings in local currency. Issuer default rating in local currency reflects probability of default on debt issued (with benefits) in national currency of country; issuer default rating in foreign currency is estimate of credit risk on debt issued in foreign currencies. Typically, sovereign rating of issuer is in line with particular type of debt rating that most accurately characterizes degree of creditworthiness.

Table 4

Defining the indicative sovereign rating based on quantitative assessments of political and economic environment, as well as financial system stability in S&P

In some cases, defaults on government-guaranteed obligations can be considered as ranking event. In particular, in presence of significant amounts of such debt to total public debt, sovereign issuer default rating could be lowered to level of RD (Restricted Default). Instead, default of issuer, which is 100% state owned and/or is under total state control, not usually regarded as event of sovereign default, even if default is direct result of sovereign issuer actions. Responsibility of sovereign issuer as any other shareholder is limited and does not guarantee that all creditors will receive compensation.

We should noted that, given existence of political, non-financial relationships between sovereign issuers and official creditors, non sovereign issuer obligations to other states and official creditors, including international organizations such as the International Monetary Fund and World Bank, will not lead to decrease of sovereign issuer default rating to level D or RD. However, if arrears to official creditors point to growing financial problems or lack of willingness to pay, it is taken into account in determining rating of sovereign issuer default. Moreover, official creditors may seek to obtain same conditions as private creditors in restructuring their claims, especially in the Paris Club of creditors. Therefore, in case of default to private creditors (such as commercial bank loans), which are not rated and if amount of such arrears will be significant, sovereign issuer rating is assigned to RD.

Also RD rating is assigned in case of an exchange of rated troubled sovereign debt. If, according to Fitch, announced exchange will be exchange of problem debt, sovereign issuer default rating will be lowered to level C, indicating high probability of default in near future. Securities ratings, subjected to such exchange, will be also reduced to level of C.

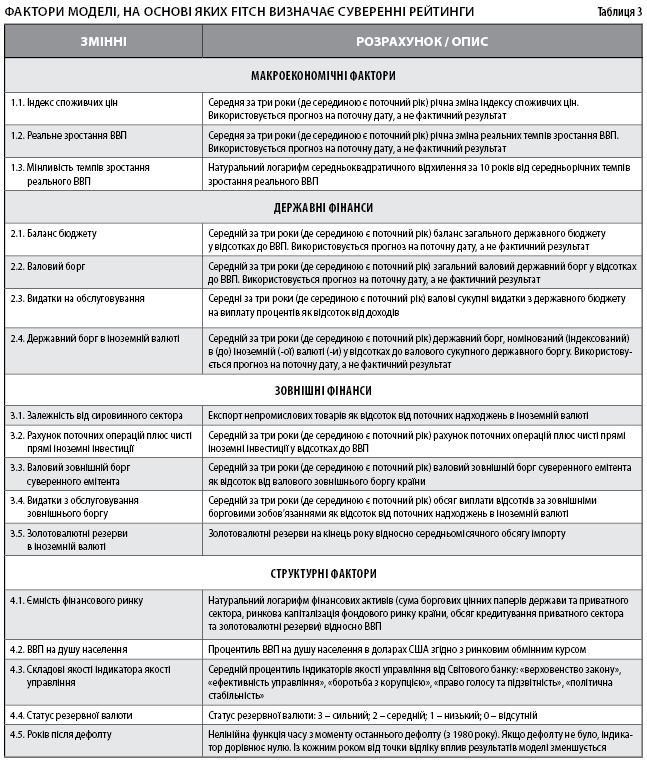

Once an offer to exchange was made and after receiving confirmation that exchange will take place (for example, because it was carried out with minimum level of participation in exchange), Fitch will assign default sovereign issuer rating - RD. Ratings of securities to be exchanged will be lowered to D and remain at that level until sovereign issuer is eligible with RD. Securities ratings that are not exchanged and are serviced in future, remain at C before exchange is completed. Later they get ratings according to their priority in new structure of liabilities after exchange. After sharing problem obligations sovereign issuer default rating is likely to be upgraded from RD to level appropriate to sovereign issuer prospects. Ratings defaulting sovereign issuers are based on results of model, consisting of 17 factors (Table 5).

Table 5

Factors model on which Fitch defines sovereign ratings

As shown in factors detailed structure, according to which ratings of sovereign obligations are determined, performance level of debt and its structure is significant, but not determinative factor of credit rating. For Ukraine, low GDP per capita is the main limiting factor in assigning credit rating of sovereign obligations, as well as economic structure, export liquidity rates, budget and contingent liabilities, low capacity of domestic financial market and political risks. Accordingly, low ratings for these factors in Ukraine should be offset by prudent and conservative debt policy.

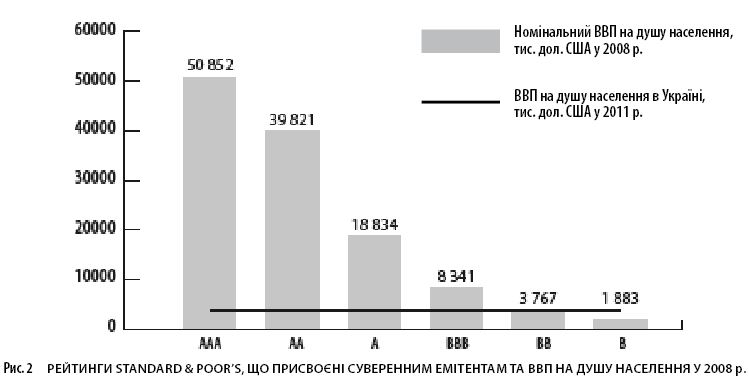

Most of these factors are interdependent, and GDP per capita can be the one of integrated indicators. As shown in Fig. 2, there is clear ratings dependence on GDP per capita. There are very few cases in world where sovereign rating of country for more than two positions deviates from the rating assigned according to GDP per capita (including China, India).

Fig. 2. Standard & Poor's ratings, assigned to sovereign issuers and GDP per capita in 2008

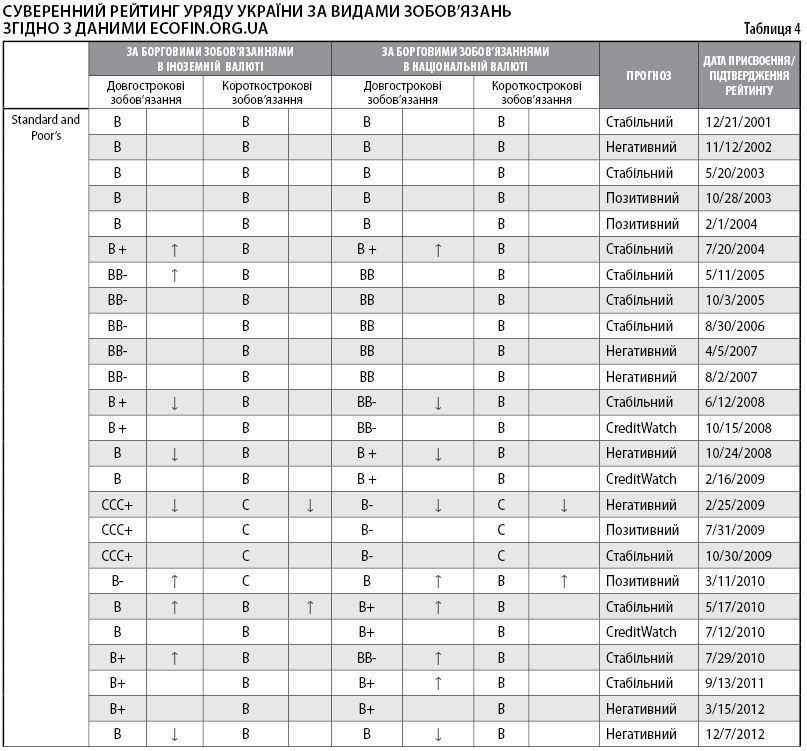

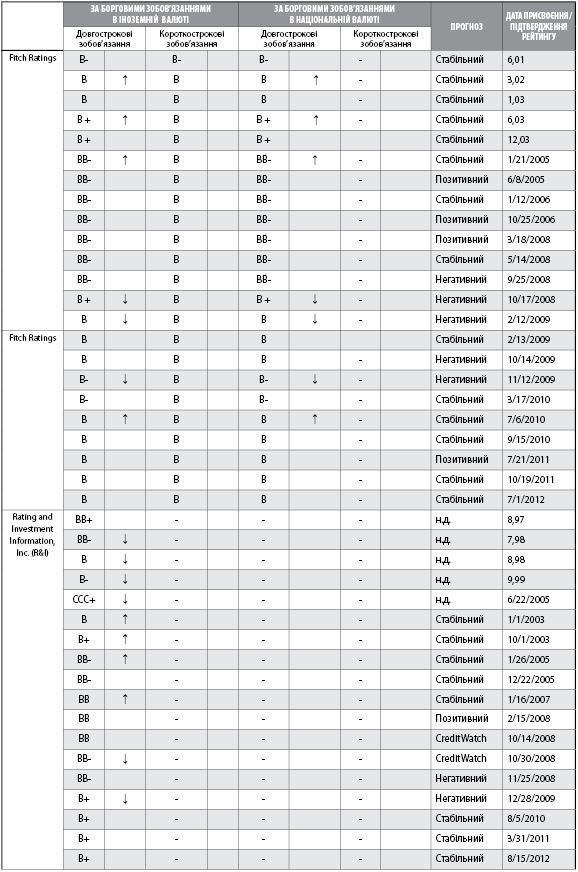

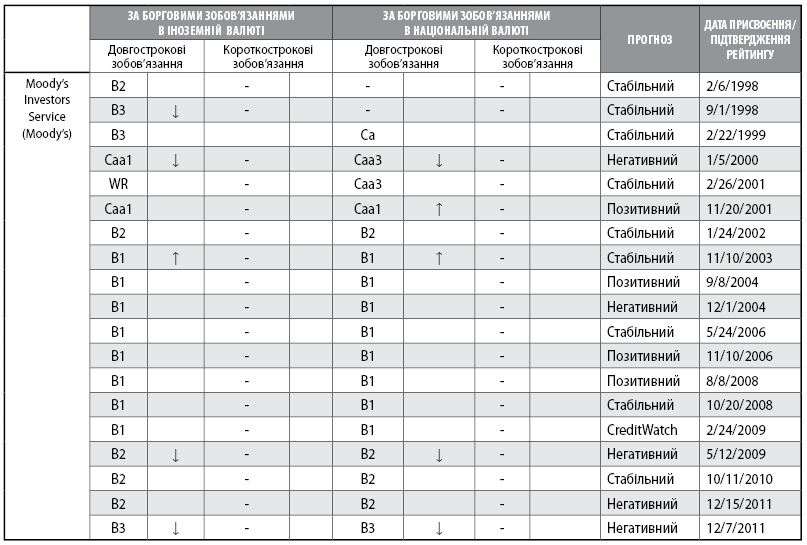

Table 6 shows ratings for Ukrainian government debt by international rating agencies. Notably, since 1998, Ukraine has never got sovereign rating higher than BB.

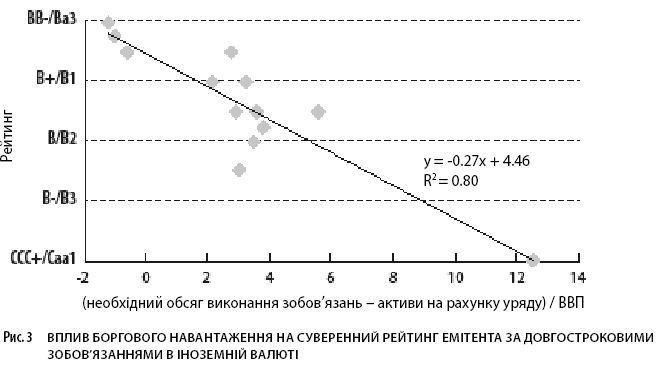

Impact of debt burden indicators on credit rating was carried out by following procedure. Since 2000, rating value on long-term liabilities in foreign currency are converted into digital form from 1 (CCC + / Caa1) to 6 (BB/Ba3). If in relevant two categories year awarded, rating takes into account end of year, if three - the average in year. Then average rating value is determined according to four international rating agencies.

Rate of necessary level for net assets commitment in government accounts at the beginning of year is taken as an explanatory variable. As shown in Fig. 3, statistics are divided into three groups. First reflects that, if necessary amount of debt and public debt is less than amount of cash assets at the beginning of relevant year, probability of assigning sovereign rating on liabilities in foreign currency is above B+/B1 and below BB-/Ba3 rating, and is 80%. The second says that if required level of debt and public debt minus cash assets at the beginning of respective year varies from 2 to 6% of GDP, there is high probability of assigning rating from B/B2 to B+/B1. And at corresponding figure value below 12% of GDP, default rating CCC + / Caa1 is assigned.

Fig. 3. Impact of debt burden on sovereign issuer rating for long-term liabilities in foreign currency

Main